Insurance coverage for inpatient rehab is real, but it is rarely simple or automatic.

Most commercial plans, Medicaid programs, and Medicare cover at least some substance use disorder treatment, and federal parity law prohibits insurers from treating behavioral health benefits more restrictively than comparable medical care.

This article walks you through exactly what is covered, what is not, and what to expect from the approval process so you can plan ahead with confidence.

Does Insurance Cover Inpatient Rehab?

Yes, insurance commonly covers inpatient rehab and many residential treatment services, but coverage depends heavily on your plan type, the level of care, and whether the insurer finds treatment medically necessary.

About 5.7 million Medicare beneficiaries alone have a substance use disorder, yet fewer than one in four receive treatment, which shows just how large the gap between formal coverage and real access can be.

The short answer is that most people with private insurance, Medicaid, or Medicare can get some form of inpatient or residential substance use disorder treatment covered.

The longer answer is that the level of care, the setting, and the insurer’s utilization management rules all shape what you actually receive.

What Levels of Care Does Insurance Usually Cover?

Before looking at specific payers, it helps to understand the main levels of care and how insurers treat each one.

- Inpatient hospital-based treatment is 24-hour structured care in a hospital or similarly acute setting. This is covered across commercial insurance, Medicaid, and Medicare when medically necessary.

- Withdrawal management or detox addresses the acute medical risks of stopping alcohol or other substances. Washington state law now bars prior authorization during the first three calendar days of withdrawal management for affected plans, reflecting how urgent this level of care is.

- Residential treatment is live-in, non-hospital care with structured daily therapy and monitoring. This is the most contested category: often covered by commercial and Medicaid plans, but generally not covered by Medicare.

- Partial hospitalization programs (PHP) are intensive day programs. Medicare and most commercial plans cover PHP in appropriate circumstances.

- Intensive outpatient programs (IOP) are structured outpatient programs requiring at least nine hours of services per week. Medicare began covering IOP on January 1, 2024, closing a significant gap in the continuum of care.

- Standard outpatient therapy and medication treatment are the most widely covered services, though prior authorization and network barriers still create friction.

The table below summarizes how the three main payers typically treat each level of care.

| Rehab service | Commercial insurance | Medicaid | Medicare |

|---|---|---|---|

| Inpatient hospital-based treatment | Usually covered | Often covered | Covered when medically necessary |

| Withdrawal management or detox | Usually covered | Often covered | Covered in appropriate settings |

| Residential SUD treatment | Often covered, but variable | Often covered | Generally not covered |

| Partial hospitalization (PHP) | Usually covered | Often covered | Covered |

| Intensive outpatient (IOP) | Usually covered | Often covered | Covered since 2024 |

| Standard outpatient therapy | Usually covered | Usually covered | Usually covered |

| Medication-assisted treatment | Usually covered | Usually covered | Covered through multiple pathways |

Does Insurance Cover Residential Treatment?

Residential treatment sits in an awkward middle ground. It is more intensive than outpatient care but less medically acute than hospital-based inpatient care, and that ambiguity has historically made it the most disputed coverage category.

For commercial insurance and Medicaid, residential treatment is often covered, especially where state parity and access laws are strong.

The 2024 federal MHPAEA final rule framework suggests that a plan covering inpatient care for medical conditions but excluding residential treatment for substance use disorder may create a parity violation, because the exclusion applies only to behavioral health. That legal pressure is pushing more commercial plans toward coverage.

For Medicare, the picture is different. Medicare covers inpatient treatment, outpatient care, PHP, and IOP, but does not cover residential SUD treatment programs.

The Legal Action Center states that Congress must authorize residential SUD coverage in Medicare, meaning the gap is statutory rather than administrative. Until that changes, Medicare beneficiaries who need residential care face a real hole in their coverage.

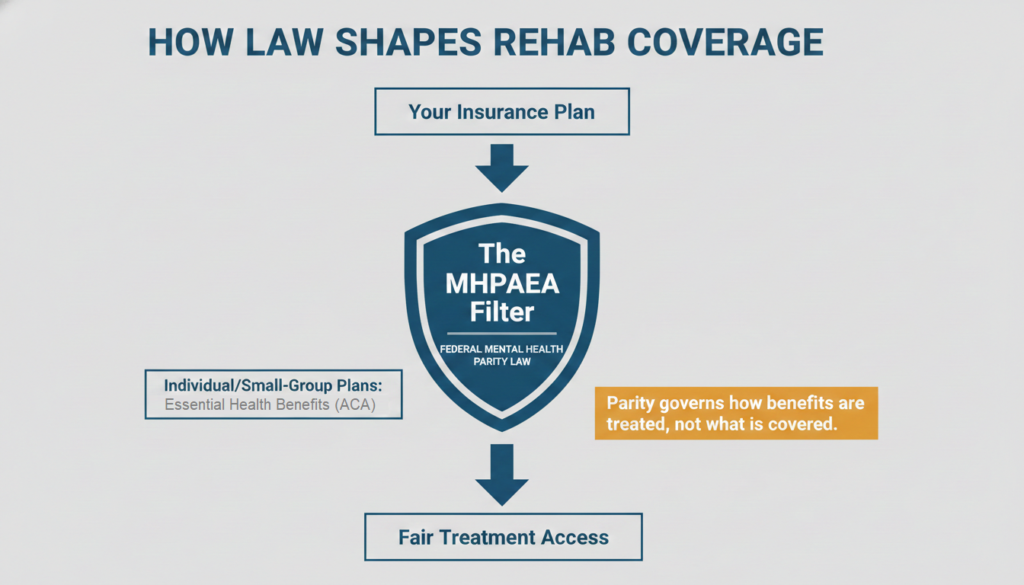

How Federal Parity Law Shapes Coverage?

The Mental Health Parity and Addiction Equity Act (MHPAEA) is the legal backbone of behavioral health coverage.

It prohibits plans that offer mental health or substance use disorder benefits from applying financial requirements or treatment limits that are more restrictive than those used for comparable medical or surgical benefits. This covers copays, day limits, prior authorization, reimbursement methods, and network composition.

The federal parity regulations at 45 C.F.R. § 146.136 make clear that nonquantitative treatment limitations, including prior authorization and medical management standards, must be applied comparably and no more stringently to behavioral health benefits than to medical or surgical benefits.

That matters directly for inpatient alcohol and drug rehab, where short initial authorizations and aggressive concurrent review are common.

One important nuance: parity law does not itself require every plan to cover every rehab service. It governs how covered benefits must be treated.

The Affordable Care Act fills part of that gap by requiring mental health and substance use disorder services as essential health benefits in non-grandfathered individual and small-group plans.

In May 2025, federal agencies announced they would not enforce the newer portions of the 2024 MHPAEA final rule while litigation is pending, plus an additional 18 months. Parity protections are not gone, but the stronger enforcement framework is partially paused. That makes state-level reforms especially important right now.

What Washington State Shows Us About Strong Coverage Rules?

Washington provides the clearest current example of what meaningful insurance coverage looks like when state law goes beyond abstract parity language into concrete operational rules.

Beginning January 1, 2025, Washington’s Senate Bill 6228 created specific protections for inpatient and residential SUD treatment. According to Premera’s provider guidance summarizing the law, affected fully insured commercial plans must follow these rules:

- No prior authorization during the first two business days of inpatient or residential SUD treatment

- No prior authorization during the first three calendar days of withdrawal management

- Authorization must cover a minimum 14-day period from the start of treatment

- Any subsequent authorization must cover a minimum of seven days

- Plans may not consider a person’s length of stay at a behavioral health agency when authorizing continuing care

- Plans may not find a lack of medical necessity based primarily on length of abstinence, and abstinence due to incarceration or hospitalization cannot be counted against the patient

Washington also updated its Mental Health Parity Act in 2025 to align with the federal MHPAEA rules and requires that utilization and clinical review criteria be consistent with generally accepted standards of care. The Washington Office of the Insurance Commissioner oversees compliance and parity reporting.

These rules matter beyond Washington because they show what is possible. The most effective reforms are not vague mandates to cover behavioral health. They are specific operational rules that target the exact utilization management barriers that most often keep people from using the care they are entitled to.

Medicare’s 2024 IOP Expansion: A Major Step Forward

One of the most significant recent changes in rehab coverage is Medicare’s addition of IOP benefits, effective January 1, 2024. Before this change, Medicare beneficiaries often fell into a gap between standard outpatient therapy and the more intensive PHP or inpatient levels of care.

The CMS final rule for CY 2024 established payment for IOP services in hospital outpatient departments, community mental health centers, federally qualified health centers, rural health clinics, and opioid treatment programs.

A physician must determine that the patient needs at least nine hours of IOP services per week, and that determination must be reviewed at least every other month.

The Center for Health Care Strategies notes that before 2024, IOP was primarily covered by Medicaid and private insurance, while Medicare-only beneficiaries often lacked access.

That gap is now closed for most settings, though freestanding SUD treatment facilities are still not broadly covered under Medicare, and in-person requirements may limit virtual IOP access.

Prior Authorization: The Real Gatekeeper

Even when a rehab service is formally covered, prior authorization is often the decisive factor in whether care actually happens. For higher-intensity services including residential treatment, PHP, and IOP, prior authorization and concurrent review are nearly universal.

Failure to obtain or extend prior authorization is one of the most common causes of preventable denials in addiction treatment.

Insurers typically require clinical documentation showing that the requested level of care is medically necessary, often using criteria aligned with the American Society of Addiction Medicine (ASAM) framework. Washington’s 2025 rules require health plans to use ASAM criteria, fourth edition, no later than January 1, 2026.

Concurrent review means the insurer reassesses medical necessity repeatedly during a stay. A plan may have no formal day cap on inpatient care and still tightly manage length of stay through serial short authorizations.

That is why asking whether insurance covers 30 or 90 days is the wrong starting question. The better question is how long the insurer will continue to find the current level of care medically necessary based on ongoing clinical documentation.

What Out-of-Pocket Costs Should You Expect?

Coverage does not mean zero cost. Your actual financial exposure depends on several interacting factors.

If you have not yet met your deductible, you will pay that amount first before the insurer begins sharing costs. After the deductible, coinsurance applies, typically ranging from 10 to 50 percent depending on your plan tier and network status.

Some plans also charge a per-confinement copay for each inpatient admission. Once you reach your annual out-of-pocket maximum, the plan covers 100 percent of allowed costs for covered in-network services for the rest of the year.

Network status has an outsized effect on cost. Behavioral health patients use out-of-network providers about three times more often than patients seeking physical care, and mental health professionals are reimbursed for office visits about 20 percent less than medical professionals.

That reimbursement gap drives network inadequacy, which in turn pushes patients toward more expensive out-of-network options.

If the facility you need is out-of-network, ask whether a Single Case Agreement is possible. This is an arrangement where the insurer agrees to treat an out-of-network facility as in-network for a specific stay, usually when no suitable in-network option is available or when the facility offers services not reasonably available in-network.

Detox, psychiatry, lab work, and medications are often billed separately from the residential stay itself, so your final cost may include multiple claim lines even when the stay itself is covered.

When Coverage is Denied: Appeals and Parity Arguments

Denials happen, but they are not always final. If your insurer denies inpatient or residential rehab, you can request an internal review and submit updated clinical documentation.

If the internal appeal fails, external review through an independent third party may be available depending on your plan and state.

Appeals are stronger when they include current clinical documentation, evidence of failed lower levels of care, documented withdrawal or safety risks, co-occurring conditions, and, where relevant, a parity-based argument.

If the denial reflects a restriction applied only to behavioral health and not to comparable medical or surgical care, that may be grounds for a parity challenge.

State parity enforcement actions tracked across more than 30 plans have resulted in over 31 million dollars in fines and related payments over six years, covering issues including improper prior authorization for medication-assisted treatment, reimbursement disparities, and network adequacy failures. That record shows parity arguments have real teeth when pursued.

The Gap Between Legal Coverage and Real Access

The most important insight across all the evidence is this: legal coverage and practical access are not the same thing.

A plan may formally cover residential treatment while making it nearly impossible to use through short authorization windows, narrow networks, low reimbursement rates, or restrictive medical necessity criteria.

Overdose deaths among adults age 65 and older have quadrupled over two decades, and over 6.3 million Medicare beneficiaries had an alcohol or drug use disorder in 2022.

Those numbers make the coverage gap in Medicare residential treatment more than a policy abstraction. They represent real people who cannot access a level of care that commercial and Medicaid plans often cover.

The most meaningful coverage protections are not broad promises but specific operational rules: no early prior authorization, minimum authorization periods, restrictions on abstinence-based denials, and network and reimbursement oversight.

Where those rules exist and are enforced, coverage works. Where they do not, even a nominally generous benefit can be inaccessible in practice.

If you or someone you care about is ready to take the next step, our team at Thoroughbred Wellness and Recovery can walk you through your options and verify your benefits quickly. So, reach out today to learn more about our residential and inpatient rehab programs and how we can help you move forward.