Paying for intensive mental health or substance use treatment can feel overwhelming, especially when you’re already navigating a crisis.

Most insured adults who attend a Partial Hospitalization Program in 2025 paid tens to low hundreds of dollars per day in coinsurance after meeting part of their deductible, with total out‑of‑pocket costs for a typical 5 to 10 day episode ranging from the low hundreds to low thousands of dollars.

This article explains how PHP is billed, what Medicare and commercial plans actually pay, and which factors drive your final cost so you can plan ahead with confidence.

What is a Partial Hospitalization Program and How Is It Paid?

A Partial Hospitalization Program is an intensive, structured outpatient behavioral health service designed as an alternative to inpatient psychiatric hospitalization.

Under Medicare’s Outpatient Prospective Payment System, PHP is paid on a per diem basis, bundling multiple therapy and support services into a single daily payment.

To qualify, programs must provide at least 20 hours of PHP services per week and deliver a minimum of three covered services each day.

Medicare distinguishes two payment tiers per provider type: one for days with three services and one for days with four or more services. This structure rewards higher daily intensity and reflects the resource demands of running a comprehensive program.

For calendar year 2025, CMS maintained this framework using claims from 2023 and recent cost reports to set rates.

The 2026 proposed rule continues the same approach with updated data, ensuring stability for hospitals, community mental health centers, and patients alike.

Why per diem bundling matters to you?

Because PHP is adjudicated per day once the service intensity threshold is met, your liability is assessed against one allowed amount per day rather than dozens of separate therapy lines.

This collapses cost sharing into a smaller number of daily events and limits the chance that small coding errors trigger separate denials and surprise bills.

Commercial policies that mirror per diem bundling reinforce this predictability, making it easier to estimate your total episode cost upfront.

How Medicare Pays for PHP and What Beneficiaries Owe?

Medicare sets PHP rates through the OPPS using geometric mean costs and relative weights derived from hospital claims and cost report data.

For 2025, the methodology used CY 2023 claims; for 2026, CMS proposes using CY 2024 claims with normalization to a benchmark Ambulatory Payment Classification.

Although the fact sheets do not list dollar rates in their summaries, the method ensures that PHP payments are grounded in observed hospital cost patterns and scaled consistently across APCs.

Deductible and coinsurance rules

For Medicare PHP, the outpatient mental health treatment limitation does not apply. However, the Part B deductible and 20 percent coinsurance do apply.

In practice, your out‑of‑pocket per day is any remaining Part B deductible if not yet met in the calendar year, plus 20 percent of the Medicare allowed per diem for that day.

Coinsurance applies whether the day is classified in the three services APC or the four or more services APC; allowed amounts differ by APC, so raw dollar coinsurance will vary.

Beneficiaries who carry a Medicare Supplement or have secondary coverage may see further reductions in their net out‑of‑pocket.

If you have fully met the Part B deductible, a hypothetical allowed per diem of $400 would yield $80 in coinsurance, while a $600 per diem would yield $120. For a 10 day episode with an even split of day types, coinsurance would be roughly $1,000 to $1,200 total.

How Commercial Plans Pay for PHP and What Members Owe?

Commercial policies often align with the per diem concept. For example, Blue Cross NC specifies that PHP codes H0035 or S0201 are allowed on facility claims as a per diem and include all facility, professional, ancillary, and other services rendered to the member.

This explicitly signals that member cost sharing is assessed against one bundled daily amount, rather than piecemeal CPTs.

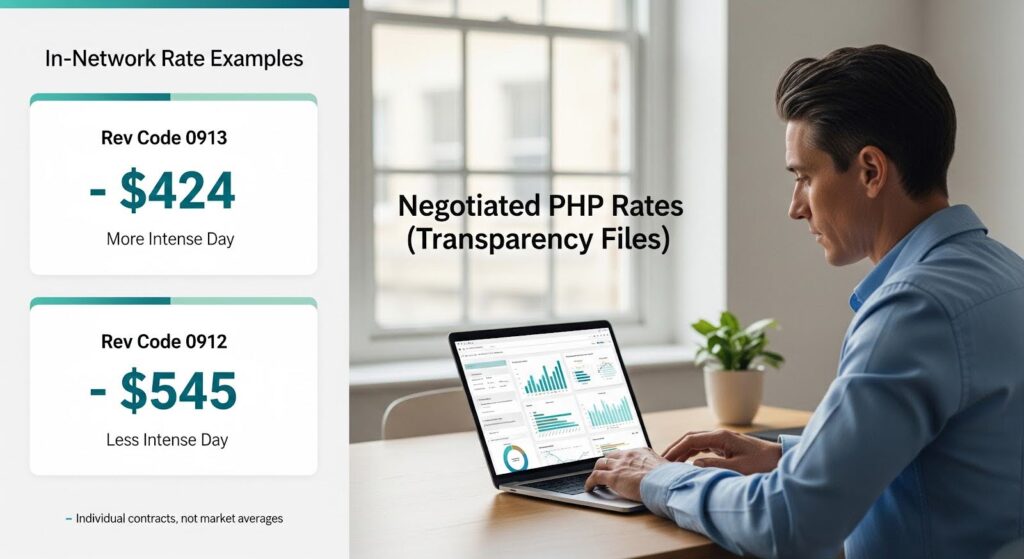

That policy also maps commonly used revenue codes such as 0912 and 0913 to less or more intense partial hospitalization day types, similar in spirit to Medicare’s three versus four or more services APCs.

Negotiated rate transparency snapshots

Under federal Transparency in Coverage rules, payers publish in network negotiated rates via machine readable files. Third party aggregators display these data.

For PHP like revenue codes, examples visible in 2025 to 2026 files illustrate the order of magnitude. For revenue code 0913, often used commercially for more intense partial hospitalization, a UnitedHealthcare negotiated rate of $424.00 is displayed for a Massachusetts provider.

For revenue code 0912, often used commercially for less intense partial hospitalization, a UnitedHealthcare negotiated rate of $545.00 is displayed for a California psychiatric hospital.

These are individual contract examples, not averages, and do not reflect all markets, payers, or facility types. They do, however, anchor plausible member cost sharing calculations for 2025 in the absence of public cash or self pay rates. Members subject to deductibles and coinsurance would cost share against these allowed amounts.

Marketplace cost caps and cost sharing reductions

ACA Marketplace plans cap annual in network out‑of‑pocket for essential health benefits. In 2025, the maximum out‑of‑pocket was $9,200 for an individual and $18,400 for a family. After you reach this MOOP, the plan pays 100 percent of covered in network services.

Enrollees eligible for cost sharing reductions in silver plan variants have substantially lower MOOPs, providing important protection for low and moderate income patients who require multi day PHP episodes.

Worked Examples of Commercial Out‑of‑Pocket Costs

To illustrate 2025 commercial out‑of‑pocket mechanics, we combine the per diem concept with observed allowed amount examples from transparency files. These are illustrative only.

Scenario A: Employer plan with deductible remaining

Allowed amount per day: $450. Member status: $1,000 deductible remaining; 20 percent coinsurance afterward.

Day 1: $450 applied to deductible. Days 2 and 3: $550 remaining deductible plus 20 percent of each day’s remainder. Five day episode out‑of‑pocket: approximately $1,450. Exact sequencing depends on deductible met timing.

Scenario B: Employer plan with deductible met

Allowed amount per day: $550. Member status: deductible met; 20 percent coinsurance. Out‑of‑pocket per day: $110. Five day episode out‑of‑pocket: $550. Per diem bundling simplifies forecasting.

Scenario C: Marketplace silver plan

Allowed amount per day: $500. Member status: deductible met; 30 percent coinsurance; MOOP far from reached. Out‑of‑pocket per day: $150. Five day episode out‑of‑pocket: $750. CSR variants may yield lower coinsurance or MOOP.

Scenario D: Marketplace silver plan near MOOP

Allowed amount per day: $500. Member status: only $300 left to MOOP. Days 1 and 2: $150 each. Day 3 onward: $0 after MOOP. Five day episode out‑of‑pocket: $300. After MOOP, no further out‑of‑pocket for covered in network care.

These examples show how per diem allowed amounts in the low to mid hundreds of dollars map into per day coinsurance in the tens to low hundreds of dollars. Total episode out‑of‑pocket scales with the number of days and your proximity to the deductible and MOOP.

Medicaid Coverage and Out‑of‑Pocket Expectations

Medicaid PHP coverage and member cost sharing are state specific. State fee schedules and managed care contracts determine provider reimbursement; many Medicaid programs apply nominal or zero cost sharing for intensive behavioral health services, but details vary.

For example, California’s Medi Cal Day Services rates and other behavioral health fee schedules are publicly posted, though our citations focus on payer reimbursements rather than beneficiary out‑of‑pocket.

Patients and providers should consult the specific Medicaid plan’s member materials for 2025 cost sharing rules.

As a general matter, Medicaid imposes strict limits on cost sharing for low income enrollees, making PHP more financially accessible than commercial or Medicare coverage for eligible individuals.

Uninsured and Self‑Pay: Bounding a Difficult‑to‑Observe Market

Self pay PHP prices are not consistently published. Unlike in network negotiated rates required in machine readable files, hospitals and community mental health centers are not uniformly posting PHP cash prices in easily comparable formats.

However, MRFs provide a floor for expectations. When negotiated per diem allowed amounts for certain providers and plans are in the $400 to $550 range, uninsured cash prices may be equal to, lower than via prompt pay discounts, or higher than those amounts depending on the provider’s pricing policy.

Hospital affiliated programs frequently list higher gross charges, with self pay discounts negotiated case by case.

As of late 2025 and early 2026, CMS’s Transparency in Coverage schema 2.0, finalized October 1, 2025 with enforcement beginning February 2, 2026, did not directly compel publication of cash prices for PHP per diem.

It did, however, significantly improve the structure and comparability of negotiated rate data that can be used as a reference point in price discussions.

Patients without insurance should request a good faith estimate and ask for a self pay discount referenced to the program’s in network negotiated per diem rates for similar services.

What Changes Out‑of‑Pocket the Most?

- Deductible status dominates. If you hit PHP early in the plan year with an unmet deductible, per diem allowed amounts flow directly into out‑of‑pocket until the deductible is met. The same episode in October could cost you only coinsurance if the deductible was already met.

- Allowed amount level. A 20 percent coinsurance on $550 is $110; on $800, it is $160. Differences in contracted per diem rates across facilities and payers propagate into member out‑of‑pocket. Negotiated transparency data empower you and referring clinicians to anticipate this before admission.

- Service intensity day type. Where payers differentiate less intense and more intense days, the allowed amount can differ accordingly, similar to Medicare’s three versus four or more services APCs. You face higher dollar coinsurance on higher intensity days.

- MOOP proximity. Once you approach your MOOP, subsequent PHP days may be free at point of service for covered in network care. Conversely, early episode days accrue out‑of‑pocket until the MOOP is reached.

Policy Shifts Affecting Cost Visibility and Predictability

CMS finalized Transparency in Coverage schema version 2.0 on October 1, 2025, with enforcement beginning February 2, 2026.

Schema 2.0 tightened and clarified how payers must publish in network negotiated rates, including internal only provider group references, clearer plan level identifiers, a new setting field to distinguish inpatient versus outpatient, and clarifications around institutional versus professional billing class.

These changes made MRFs more usable for benchmarking outpatient program rates and, by extension, estimating PHP out‑of‑pocket more accurately.

CMS’s 2026 Notice of Benefit and Payment Parameters, effective January 15, 2025, introduced policies to improve consumer understanding of costs and to strengthen oversight of agents and brokers. While largely prospective for plan year 2026, these measures add context.

Marketplace enrollees considering PHP in late 2025 and 2026 are likely to benefit from clearer plan displays and standardized information that can aid cost estimation and plan selection, reducing surprise bills relative to covered in network per diem services like PHP.

CMS’s 2024 Interoperability and Prior Authorization Final Rule requires impacted payers, including QHP issuers on Federally Facilitated Exchanges, Medicaid managed care, and MA organizations, to stand up APIs and accelerate PA decision timeframes.

For PHP, where preauthorization is commonly required, better electronic PA can reduce denial risk and time to care, which in turn reduces financial exposure due to inadvertent out of network use or administratively denied days.

Why This Matters for Your Recovery?

Across Medicare and commercial markets, 2025 PHP out‑of‑pocket for most insured patients clustered at levels that, while non trivial, were far more predictable and generally lower than inpatient psychiatric hospitalization out‑of‑pocket.

This is thanks to per diem bundling and annual MOOP caps for commercial coverage. Negotiated per diem amounts observed in transparency files in the low to mid hundreds for some outpatient facilities imply coinsurance that is manageable across a typical 5 to 10 day episode for many households, especially later in the plan year after deductibles are met.

The chief equity risk resides with uninsured patients and with members who encounter authorization or network status pitfalls.

This underscores the value of 2025 to 2026 transparency, Marketplace safeguards, and interoperability reforms to reduce administrative failure modes that can trigger avoidable financial harm.

Practical Takeaways

Patients with Medicare: Expect to pay the Part B deductible if still unmet and then about 20 percent of the Medicare allowed per diem per PHP day. Ask the facility’s billing office which APC your program days typically map to and whether your Medigap or secondary plan reduces coinsurance.

Patients with employer or Marketplace plans: Verify whether PHP is subject to prior authorization and whether the intended program is in network. Ask the provider to share the payer’s publicly posted in network per diem for PHP related revenue codes as a planning benchmark. If you are near your MOOP, later days may be paid at 100 percent.

Medicaid beneficiaries: Confirm coverage and any nominal copay with your plan. Many programs minimize cost sharing for PHP.

Uninsured individuals: Request a good faith estimate and a self pay discount referenced to the program’s in network negotiated per diem rates visible in MRFs. Compare per diem across facilities; per diem bundling reduces the chance of surprise add on bills for the day’s therapies.

Providers: Standardize upfront estimates using published negotiated rates and the member’s deductible or coinsurance status. Embed PA checks early and leverage the payer’s APIs as they come online under CMS 0057 F to reduce denial related financial surprises.

If you or a loved one is considering PHP and want personalized guidance on coverage, costs, and next steps, reach out to Thoroughbred Wellness & Recovery. Our team can verify your insurance, explain your benefits, and help you start treatment with clarity and confidence.